Does This Smell Like Last Year?

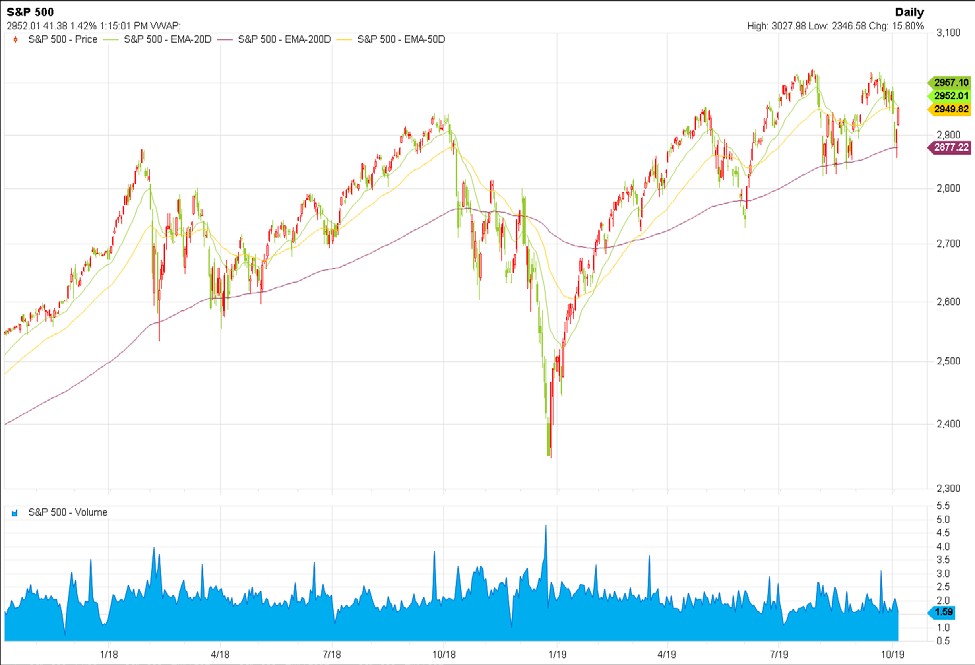

This fall kicks off the eighth quarter in a row where the major stock market averages have not been able to reach meaningfully higher levels. As of last week, the S&P 500 sits below its level from last year and is only marginally higher than its level going back 21 months to January of 2018.

You can see this from the chart below for the S&P 500.

Lately, concerns have risen and there has been a lot of short term volatility in the stock market. This is characterized by sharp single-day moves and since July 31, there have been eight days where the S&P 500 has fluctuated more than 2% in a single day.

Yet despite the daily and weekly volatility, bulls and bears face a standoff and longer-term, the market is flat. In essence, the market has been range-bound for almost two years. This means our stock market can neither reassert a long-term uptrend nor break important support levels. Each time it approaches the top end of its range it stages a hasty retreat.

John Normand, a chief analyst at JP Morgan called for a continuing of the corrective phase in the market that has been happening since August. However, he does not see a contagion of the magnitude of last year’s sell-off. Corporate earnings reports, which will start to flow this month are estimated to fall by 4%, according to Factset, and this will serve as a restraint to investment conditions.

There is certainly no shortage of challenges for the market given these economic concerns and the trade disputes that are happening. How concerned should we be?

Last year, during the fourth quarter, the market plunged 20%. Do we have to ask ourselves if this smells like last year? It is a real concern with all of the talk about a “recession”.

There is a marked difference from last year, however. In 2018, interest rates were rising amidst a slowing world economy. As a consequence, the market sickened from that condition and dropped precipitously. Today, in contrast, the Fed is lowering interest rates and making further assurances that they will be accommodative to the economy. This will probably prevent a recurrence of last year.

If the overall market continues to be stuck in a trading range, where are the opportunities to make money during the fourth quarter?

Many sectors of the stock market have seen significant declines in 2019 so these set up to be fertile areas for investment.

Names like Facebook, Amazon, Netflix, and Google are off 15% or more from their best levels from last year and have been very weak over the past several months. Many other leading software and technology companies have recently declined substantially and may be attractive longer-term. At some point, buyable bottoms will happen.

Other areas of the market have endured a horrible year which may be overdone.

Most bank stocks have retreated all the way back to levels last seen in the 2016 presidential election. These shares offer attractive relative valuations.

2019 has also been an outright disaster for energy stocks. There is a lot of upheaval happening in this industry but these companies appear to be stretched on the downside and could rebound.

One particularly strong area of the market continues to be defensive companies that are cushioned from the effects of an economic slowdown.

These companies are well-established name brands that sell food and household products. They can be good core holdings for accounts

It would also be important to stress stocks that pay dividends in this low-interest-rate environment. Steady dividend income is an important component of an investment account.

Disturbing stock market volatility in the context of the drop last year is unnerving but current conditions suggest the stock market will remain within its current trading range.

There will be more forthcoming with your third-quarter report.

Dan Botti

10/7/19

Peregrine Asset Advisers ● 9755 SW Barnes Rd. Suite 295 ● Portland Oregon 97225

503.459.4651 ● 800.278.1420 ● www.peregrineaa.com